On this page

Quick Commerce Market Share by Company: Top Players, Regional Leaders, and Market Data

WebbyCrown

March 9, 2026 • 13 min read

Quick commerce market share by company is usually measured through order share, gross merchandise value, gross order value, or revenue within the ultrafast delivery segment.

Unlike traditional e commerce, which typically offers longer delivery windows and broader inventory, and brick and mortar stores, which struggle to match the speed, convenience, and discounts of online platforms, quick commerce stands out by providing rapid access to essentials.

In most industry coverage, quick commerce refers to delivery of groceries, essentials, and convenience items in minutes, often through dark stores or highly localized fulfillment networks.

To understand the systems behind these models, see the Quick Commerce Tech Stack (OMS/WMS/TMS, inventory, dispatch, tracking, and KPIs).

Q-commerce, or the quick commerce model, is a business model that delivers groceries and other daily essentials to customers within a short time frame, usually 10-30 minutes.

For role clarity across the stack, read OMS vs WMS vs TMS in Quick Commerce to see what each system owns and how order status flows end-to-end.

The primary aim of quick commerce is to satisfy the growing consumer demand for rapid order fulfillment and ease of accessibility.

Flexible payment options are also influencing online shopping behavior, with services such as PayPal Pay in 4 allowing customers to split purchases into smaller payments while shopping online.

The global q commerce market is projected to reach over USD 350 billion by 2030.

To understand how digital commerce ecosystems evolve globally, you can also examine the broader Amazon e-commerce market share worldwide, which shows how large platforms influence global online retail competition.

The quick commerce market was valued at USD 184.55 billion in 2025 and is expected to reach USD 385.36 billion by 2034, growing at a compound annual growth rate (CAGR) of 8.55% during the forecast period.

Notably, the q-commerce sector is growing faster than traditional e-commerce platforms, with a CAGR exceeding 20% in many forecasts. This rapid growth highlights the significance of the quick commerce market size and the increasing importance of this segment within the broader e-commerce industry.

Operating in a highly competitive market, quick commerce companies seek competitive advantage through faster delivery times, advanced technology, and innovative business models such as dark store networks and hyperlocal logistics. These differentiators help them stand out and capture greater quick commerce market share.

McKinsey describes instant grocery as a convenience-led model built around delivery windows of about 30 minutes or less.

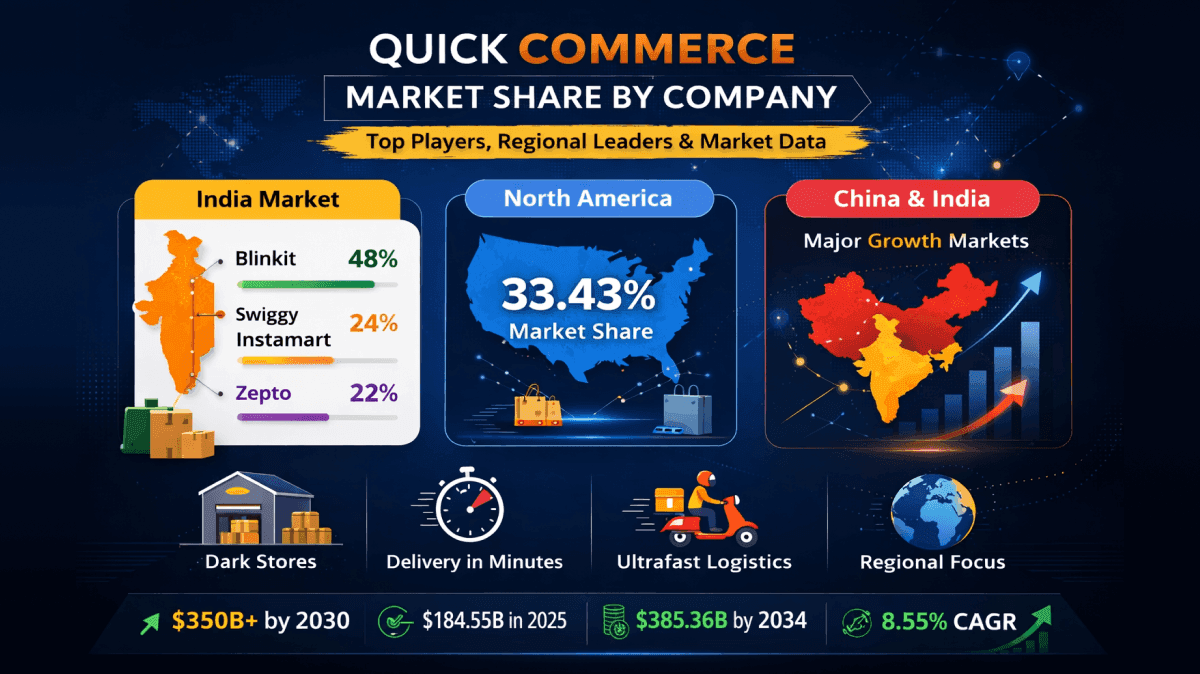

The global quick commerce market is large, but public company-by-company market-share data is not published in one universal worldwide ranking. Public sources usually show regional market size, country-level leadership, or company share within specific markets. Fortune Business Insights reports that North America held a 33.43% regional share in 2025, while Bain highlights strong quick commerce momentum in China and India.

What Quick Commerce Market Share Means

Quick commerce market share refers to the share of demand captured by a company in the ultrafast delivery segment. Depending on the source, that share may be expressed through completed orders, GMV, GOV, revenue, or user activity. Because companies and analysts do not all use the same reporting standard, quick commerce market share by company can vary by source and by metric.

Quick commerce services are segmented by delivery time frames, including instant, same-day delivery, and scheduled delivery. Same-day delivery holds a major share of the global quick commerce market, catering to the growing consumer demand for rapid delivery and immediate gratification.

The category also varies slightly across markets. Food delivery is a dominant segment within quick commerce, accounting for about 25% of the overall market share, driven by consumer demand for convenience, urbanization, and technological advances.

Groceries and other household essentials are also key product categories, with the grocery segment projected to represent 43.78% of the total market share in 2026, contributing the highest market share among all segments.

Some sources focus mainly on grocery and household essentials, while others include pharmacy, electronics, beauty, beverages, and other convenience-led categories. Fortune Business Insights identifies groceries as the leading product segment in the market, and Bain notes that FMCGs account for about half of quick commerce GMV in China.

Customer loyalty in quick commerce is driven by the speed and convenience of rapid order fulfillment, which encourages repeat purchases and strengthens a company's position in this highly competitive market. The primary aim of quick commerce is to satisfy the growing consumer demand for rapid order fulfillment and ease of accessibility.

At the operator level, share often comes down to availability and reliability—Real-Time Inventory Management in Quick Commerce explains how sellable stock, reservations, and reconciliation reduce stockouts and cancellations.

Market Drivers and Restraints in Quick Commerce

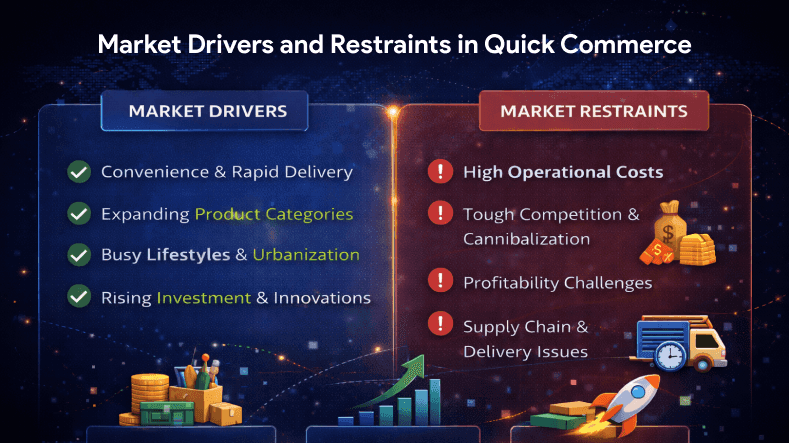

The global quick commerce market is experiencing rapid growth, propelled by a surge in consumer demand for fast delivery and instant access to everyday essentials. As urban consumers increasingly prioritize convenience and speed, quick commerce companies are leveraging advanced delivery technology and innovative business models to meet rising expectations for same-day and ultra-fast delivery.

Key Market Drivers

One of the primary drivers of the quick commerce market is the growing consumer demand for rapid delivery of groceries, household essentials, and other convenience items. The shift toward online shopping and the widespread adoption of e-commerce platforms have fundamentally changed consumer preferences, with more shoppers seeking on-demand services that offer delivery within minutes. This trend is especially pronounced in densely populated urban areas, where busy lifestyles and high population density amplify the need for swift deliveries.

Quick commerce companies are responding by investing in dark stores and micro-fulfillment centers, which enable them to reduce delivery times and optimize logistics operations. The integration of new delivery technologies, such as electric vehicles and drones, is further enhancing delivery speed and efficiency, giving companies a competitive edge in the fast-evolving commerce market.

If you’re evaluating dark-store execution, use the Dark Store WMS Checklist to validate picking, scanning, pack & stage, readiness signals, exceptions, and integrations.

Key Market Restraints

Despite its rapid expansion, the quick commerce market faces significant challenges. High operational costs remain a major restraint, as companies must invest heavily in logistics infrastructure, delivery fleets, and technology to maintain fast delivery services. The competitive landscape is intense, with numerous players vying for market share, often resulting in increased delivery costs and pressure on profit margins.

One common cost lever is batching, but it can break trust if misused—Batching Orders vs SLA Tradeoffs in Quick Commerce explains detour limits, cutoffs, late-risk protection, and KPIs.

Logistics operations in quick commerce are complex, particularly when offering same-day or instant delivery in congested urban environments. Managing delivery times and ensuring customer satisfaction can be difficult, especially as consumer expectations continue to evolve. Additionally, the need for rapid expansion and continuous investment in delivery technology can be a barrier for new entrants and smaller players.

For the last-mile decision layer, Dispatch Rider Assignment Basics in Quick Commerce covers readiness gating, rider scoring, routing, tracking signals, and KPIs for on-time delivery.

Market Outlook

Looking ahead, the quick commerce market is expected to maintain strong growth momentum during the forecast period, driven by increasing demand for on-demand delivery and ongoing advancements in delivery technology.

As consumer preferences continue to shift toward convenience and speed, quick commerce platforms will need to innovate in logistics operations, service offerings, and customer experience to stay competitive. The adoption of sustainable delivery solutions and further integration of technology will likely shape the next phase of market growth, ensuring that quick commerce remains a dynamic and essential part of the global e-commerce sector.

Quick Commerce Market Share by Company in India

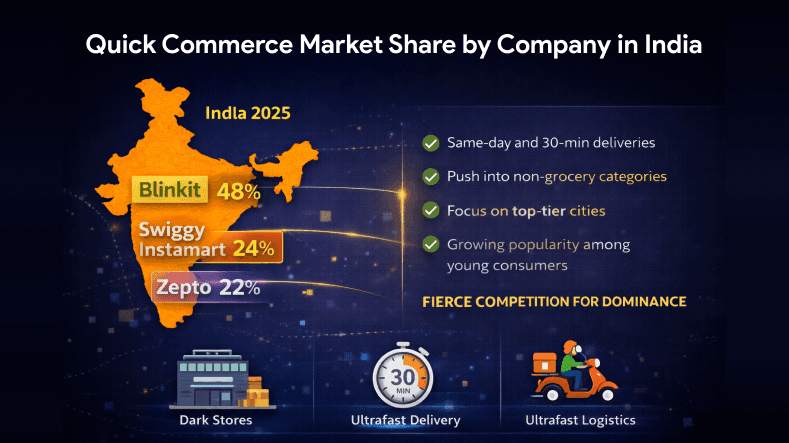

India currently has one of the clearest publicly reported quick commerce market-share snapshots by company. Reuters reported in January 2026, citing Datum Intelligence data for 2025, that Blinkit held a 48% share of India’s quick-commerce market, followed by Swiggy Instamart at 24% and Zepto at 22%. Quick commerce adoption and quick commerce market growth in India have been remarkable, with the country experiencing rapid expansion driven by increasing consumer demand and technological innovation.

Reuters also reported in March 2025 that quick commerce accounted for more than two-thirds of all 2024 e-grocery orders in India and represented a fivefold increase from 2022 in market value terms. The same Reuters report, citing Bain and Flipkart, said the segment had reached about $6 billion to $7 billion in market size and made up around 10% of India’s total e-retail spending in 2024.

India’s quick commerce company landscape is centered on Blinkit, Swiggy Instamart, and Zepto in the most widely cited public reporting. India has become one of the most competitive and fastest-growing markets for quick commerce, with major players controlling substantial market shares in this highly competitive market.

The increasing urbanization, hectic lifestyles, and the growing number of working professionals are intensifying the demand for quick access to daily necessities, driving the expansion of quick commerce services nationwide.Reuters also noted in January 2026 that the sector was valued at about $11.5 billion, showing the scale and speed of expansion in the market.

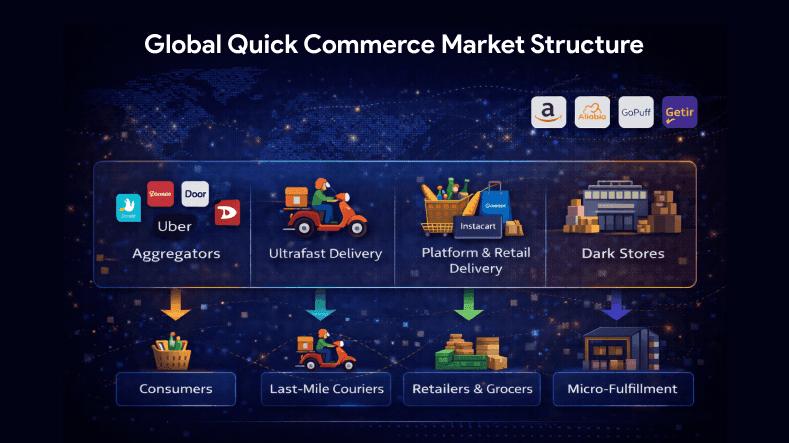

Global Quick Commerce Market Structure

The global quick commerce market is regionally fragmented. Quick commerce operations rely on maintaining strong infrastructure, such as dark stores and dependable last-mile delivery networks, to complete orders within a short time frame.

Inside the store, picking method is a major speed lever—see Batch vs Zone Picking for Quick Commerce Dark Stores for practical tradeoffs and when each method wins.

Technology integration and technological advancements, such as AI-driven inventory management and real-time demand forecasting, are crucial for optimizing quick commerce operations and improving operational efficiency.

The proliferation of smartphones and increasing internet penetration have further accelerated the growth of the quick commerce sector.

Similar technology adoption trends can be seen in software ecosystems as well, such as the design tool market share by country, where global usage patterns reflect regional digital adoption.

Public sources do not show one fixed worldwide leaderboard that applies equally across North America, Europe, India, China, and other markets. Instead, the market is shaped by local density, rider networks, urban demand, dark-store economics, and repeat convenience purchases.

Fortune Business Insights describes the market as global but regionally uneven, with North America leading by regional share in 2025. Bain’s 2025 consumer products report places China and India at the center of current quick commerce momentum in Asia.

Asia’s Role in Quick Commerce Growth

Bain reported that China’s quick commerce market was projected to reach about $120 billion to $150 billion by the end of 2025. The same Bain report stated that India’s quick commerce GMV quadrupled from 2022 to 2024.

The Asia Pacific region is anticipated to be the largest market for quick commerce, accounting for over 50% of the global market share in 2025. The quick commerce market size in the Asia-Pacific region is projected to achieve the highest compound annual growth rate (CAGR) during the forecast period, driven by factors such as dense population and accelerating urbanization. Asia-Pacific is the fastest-growing region for quick commerce due to these factors.

These figures place Asia at the center of the global quick commerce market. China contributes scale, while India contributes one of the clearest public company-share breakdowns and one of the fastest visible growth curves in the category.

North America’s Regional Market Share

Fortune Business Insights reported that North America held a 33.43% share of the quick commerce market in 2025. The same source attributes that position to strong smartphone usage, urban demand, and investment by major delivery and retail platforms.

In North America, quick commerce often overlaps with grocery delivery, same-day retail delivery, and marketplace-led local fulfillment. Because of that overlap, regional market size is more visible in public reporting than a single pure-play company ranking across the region.

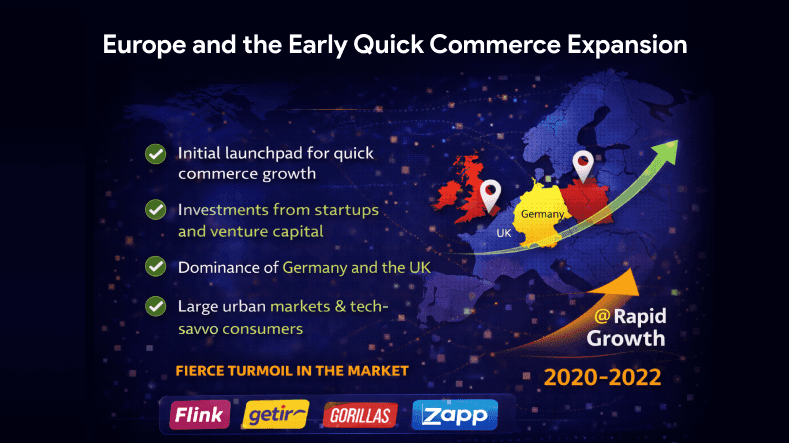

Europe and the Early Quick Commerce Expansion

Europe was one of the most visible early markets for instant grocery and quick commerce. McKinsey’s work on instant grocery described the model as centered on very fast fulfillment, dark stores, and convenience-led urban demand.

The dark store model, which uses local warehouses dedicated to online orders, has been crucial in enabling ultra-fast delivery within minutes by optimizing logistics and increasing operational efficiency for quick delivery services in Europe.

The Europe quick commerce market is projected to expand significantly, with a market size of USD 58.96 billion in 2025 and is expected to record the second-largest CAGR of 9.28% during the forecast period. Europe’s role in quick commerce is strongly associated with early platform expansion and rapid funding cycles.

Public discussions of the market later shifted toward sustainability, economics, and market consolidation as the category matured. Additionally, the European quick commerce market is experiencing increased regulation regarding sustainability and the adoption of electric delivery fleets.

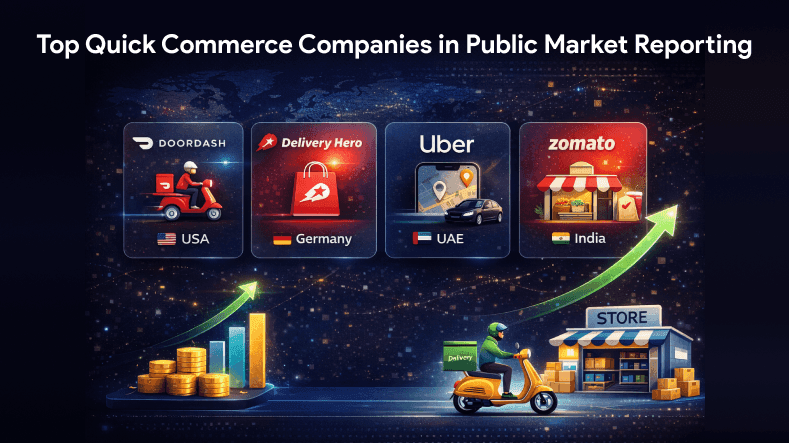

Top Quick Commerce Companies in Public Market Reporting

The most frequently cited quick commerce companies in current public reporting include Blinkit, Swiggy Instamart, and Zepto in India, along with broader historical or regional references to operators such as Getir, Flink, DoorDash, and GoPuff in discussions of quick commerce and instant grocery. Reuters’ 2025 India data clearly identifies Blinkit, Swiggy Instamart, and Zepto as the leading companies in India by market share.

These companies employ a variety of business models to achieve rapid delivery and operational scalability. For example, DoorDash operates a hybrid business model that combines third-party deliveries with partnerships with popular retailers, while Blinkit uses a hyperlocal delivery model through strategically located dark stores.

Gopuff leverages micro-fulfillment centers and dark stores to minimize delivery times to under 30 minutes, providing a significant competitive advantage. Zepto is known for its 10-minute delivery service and rapid expansion of dark stores in India, while Getir operates through dark stores to ensure delivery within 10-15 minutes for groceries and essentials.

Flink has expanded across Germany, the Netherlands, and France, acquiring Cajoo to enhance its market presence and competitive advantage.

Public company-by-company data is strongest at the country level, especially in India. Global market discussions are more often expressed through regional share, market size, and growth rates than through one unified worldwide company ranking.

FAQs

Q1.

What is quick commerce market share?

Q2.

Which company has the highest quick commerce market share in India?

Q3.

Is there a single global quick commerce market share table by company?

Q4.

Which region had the largest quick commerce market share in 2025?

Q5.

Why is India important in quick commerce?

Sources and References

This article is based on insights and data from reputable market research firms and industry experts to ensure accuracy and reliability:

- Fortune Business Insights: Provided comprehensive data on global quick commerce market size, regional shares, and market forecasts.

- Bain & Company: Offered detailed analysis of quick commerce growth, particularly in China and India, including consumer behavior and market momentum.

- McKinsey & Company: Defined key business models such as instant grocery and provided strategic insights into quick commerce operations.

- Reuters: Supplied up-to-date market share information and growth statistics for the Indian quick commerce sector.

- Research And Markets and Coherent Market Insights: Delivered market trends, forecasts, and competitive landscape overviews.

- Company Reports and Press Releases:Information from leading quick commerce companies including Blinkit, Swiggy Instamart, Zepto, DoorDash, Getir, and others was used to illustrate business models and market positioning.

- Industry Publications and Whitepapers: Additional context on e-commerce trends, logistics innovations, and delivery technologies that shape the quick commerce market.

These sources collectively underpin the article’s insights, ensuring a trustworthy and authoritative overview of the quick commerce market share and industry dynamics.

WebbyCrown's Insight

No headings found in this content.